South Africa’s residential property market continues to demonstrate strong resilience amid global economic uncertainty and shifting interest rate expectations. Stephan Potgieter, CEO of BetterHome Group Mortgage Origination and BetterBond, shares insights from the June 2026 BetterBond Property Brief.

WORDS & PHOTOS: SUPPLIED

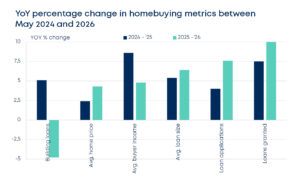

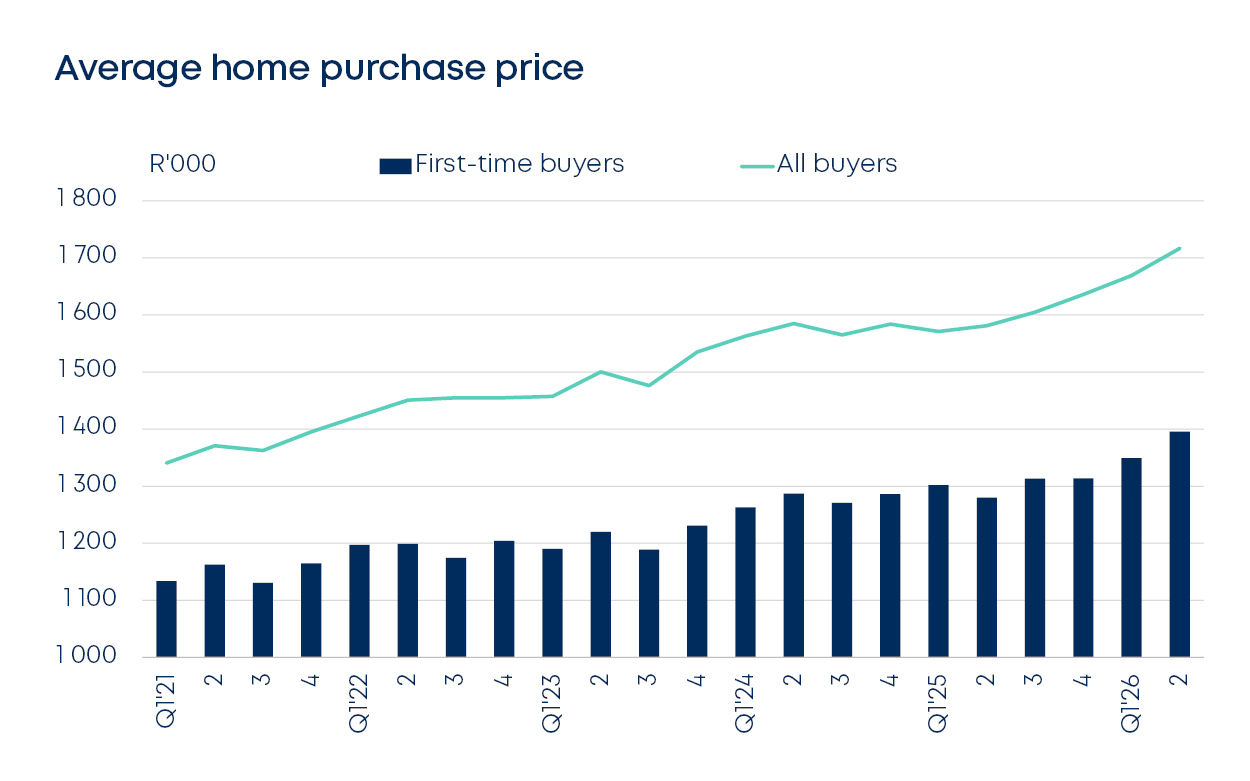

“While traditional equity markets have experienced volatility, the property sector has remained steady, with house price growth continuing to outpace inflation,” says Stephan Potgieter, CEO of BetterHome Group Mortgage Origination and BetterBond. “This stability is being driven largely by first-time buyers, whose activity has pushed house prices in this segment of the market up by 9% during the second quarter of this year.” First-time buyer homes have now reached an average price of R1.4 million, while the average house price for all buyers sits at R1.7 million.

Data from BetterBond’s latest June Property Brief shows that the listed real estate sector posted a robust 16.6% year-on-year improvement by the end of May, also outpacing inflation. This indicates continued investor interest in property, even as equities face ongoing geopolitical and macroeconomic headwinds. While the JSE All Share Index (ALSI) peaked at 130,000 points in March before retracting to 112,000 on 1 June, the property sector remained comparatively buoyant.

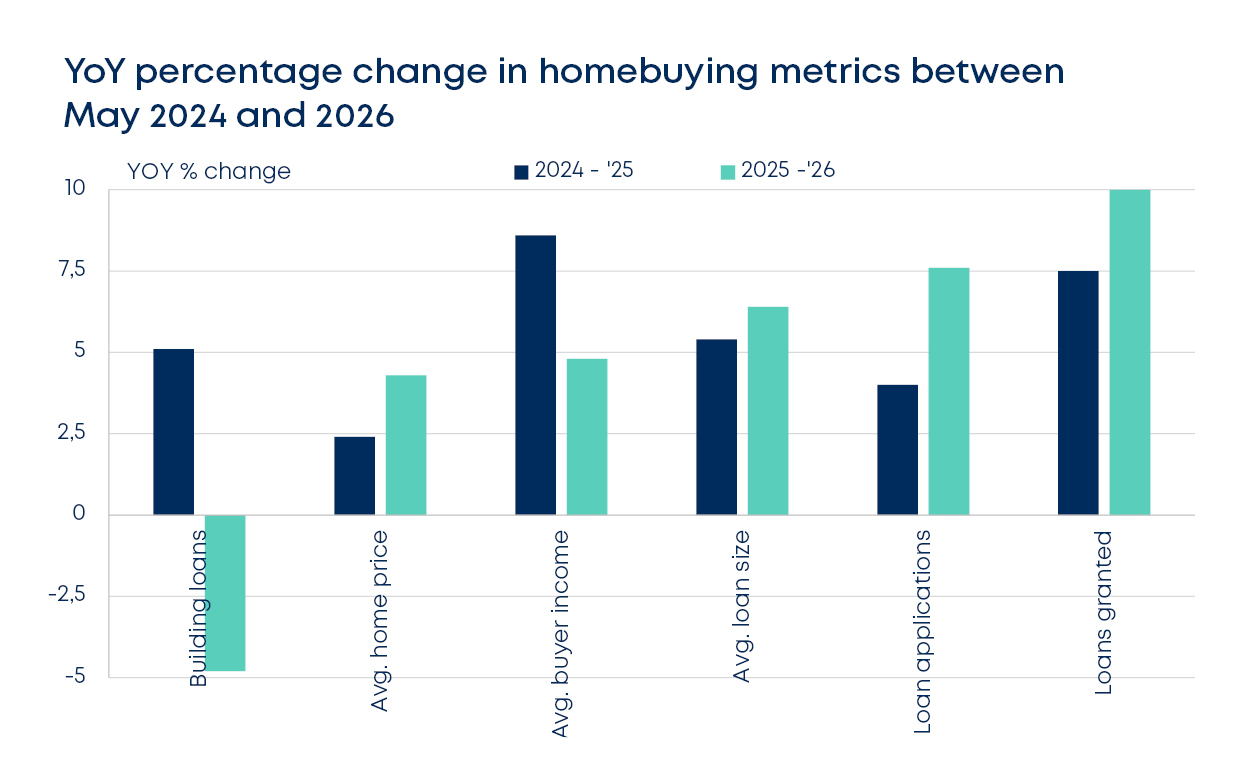

“Also significant is that this growth has occurred despite a prolonged period of elevated prime lending rates,” says Potgieter. Average home prices rose 8.6% year-on-year in the second quarter of this year, roughly double the inflation rate. Much of this momentum is being driven by resilient buyer demand, explains Potgieter. The average household income of homebuyers has reached R68 800, reflecting an average annual growth rate of 10% in real terms since the pandemic in 2020.

Regional greenshoots

While encouraging, this resilience is manifesting in different ways across the country’s regions. The Western Cape continues to stand out across key market indicators, according to BetterBond’s June Property Brief. Bond values in the province have increased by 22% over the last two years to an average of R1.6 million. The province now accounts for almost 38% of all approved building plans in the country, underscoring sustained development activity, with approved projects valued at approximately R8.5 billion.

While the value of approved building plans in the Western Cape increased by 10% year-on-year, Gauteng recorded a decline of the same margin. Meanwhile KwaZulu-Natal has shown positive movement, with the value of approved building plans increasing by 14.4% to R3.5 billion.

Coming a close second to the Western Cape, Pretoria records an average bond value of R1.3 million. However, growth here has been more moderate at 8.8% over the past two years. Mpumalanga follows with an average bond value of R1.22 million, slightly ahead of Johannesburg’s North West region.

“The North West province is proving to be a market to watch,” says Potgieter. “Bond values have increased by 18.5% to just under R1 million over the past two years, likely supported by rising prices in Platinum Group Metals (PGMs).”

Buyer behaviour

The data also reveals a “rare positive correlation” between shifts in home loan share across price segments and house price movements over the past two years, says Potgieter. Higher-priced homes have increased their share of granted home loans, with properties above R3 million rising from 9.5% to 11.4%, a 20% increase. The most active segment remains the R500 000 to R1 million band, which accounts for a third of all loans granted over the past year.

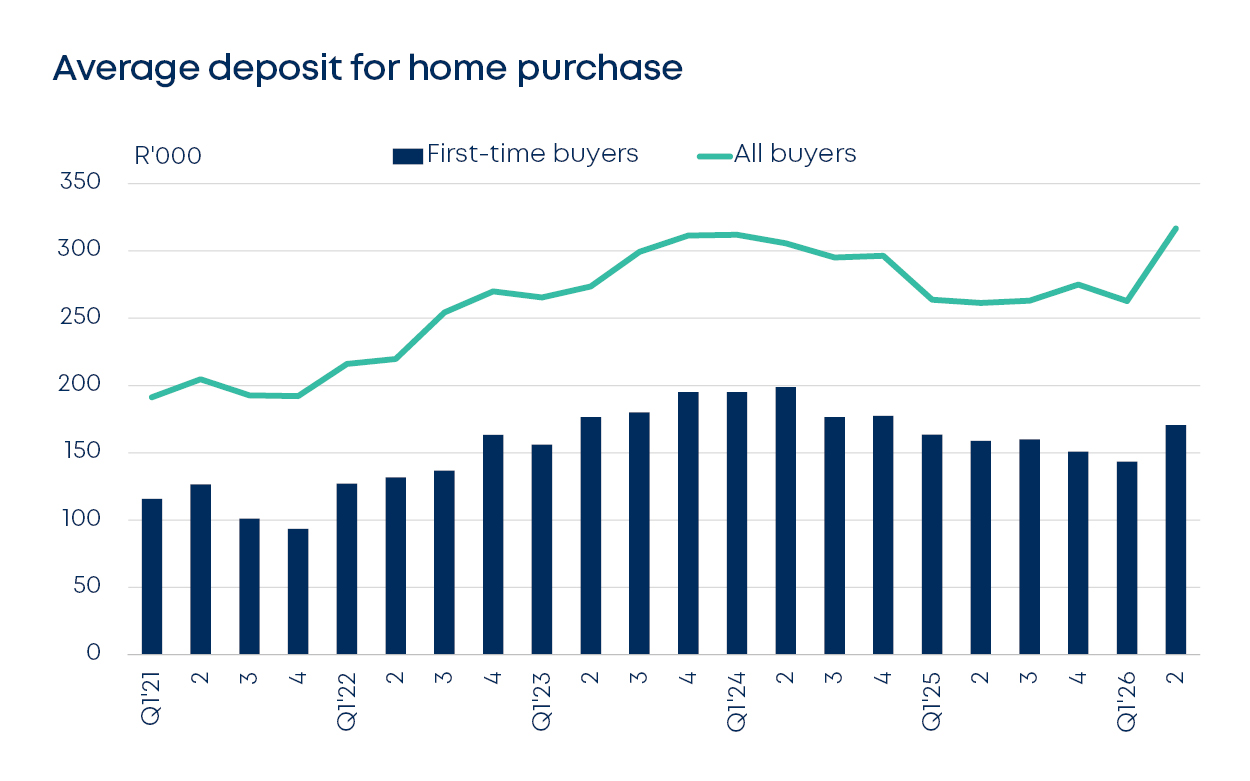

Deposit requirements shifted ahead of the anticipated return to higher interest rates, notes Potgieter. Although no further increases were recorded in May, the Property Brief does reveal that the average deposit across all buyers in the second quarter was 21% higher than in 2025. The impact has been softer for first-time buyers, who are paying 7.3% more in deposits year-on-year.

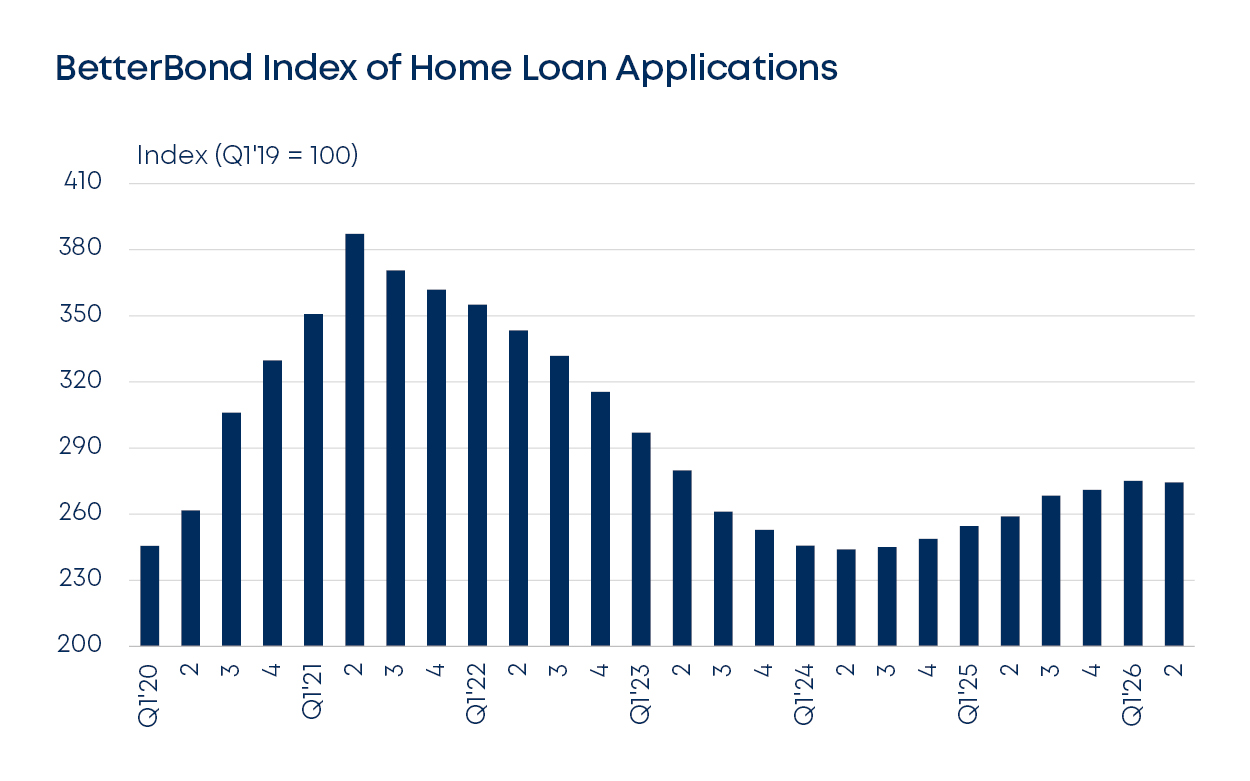

Despite the deposit increases, the decline in the BetterBond Index of Home Loan Applications in May was marginal, with year-on-year growth remaining stable at 6%. Compared with the first quarter of 2020, BetterBond still recorded 12% more home loan applications in the second quarter of this year. “Since home loan activity reached its lowest point during the extended interest rate hiking cycle that began in November 2021 and lasted 34 months, applications have since increased by 12.5%.”

Strong economic foundation

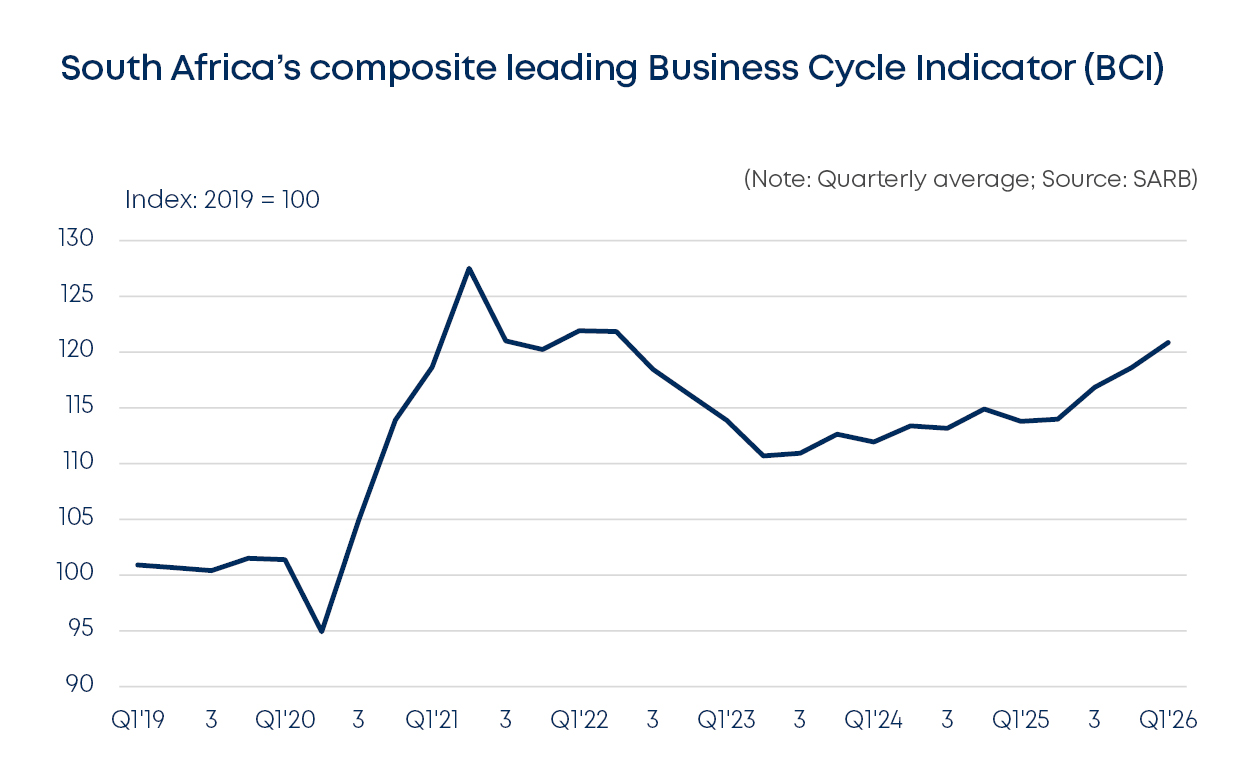

While the recent prime lending rate adjustment to 10.5% may prompt some aspirant buyers to put homebuying on hold, several indicators suggest underlying economic resilience. Leading business cycle indicators compiled by the Reserve Bank – including the commodity price index for the country’s main export commodities and number of building plans approved for flats, townhouses and houses larger than 80m² – have reached a four-year high, pointing to strengthening momentum in the broader economy, adds Potgieter.

In May, the South African rand recorded the strongest gain among major global currencies against the US dollar, appreciating by 3.5%. This contrasted with weakness in several other major currencies, including the euro, British pound, and Indian rupee, says Potgieter. Should geopolitical tensions in the Middle East ease, oil prices may also stabilise, potentially supporting a renewed interest rate cutting cycle, he adds.

With this in mind, Potgieter concludes: “First-time buyers are encouraged to make the most of this window of opportunity before lower interest rates further stimulate demand and place upward pressure on house prices.”

View the full Better Bond Property Brief June 2026 here.