Picture: The latest data from Knight Frank’s Prime Global Cities Index suggests a resilient property market in Cape Town.

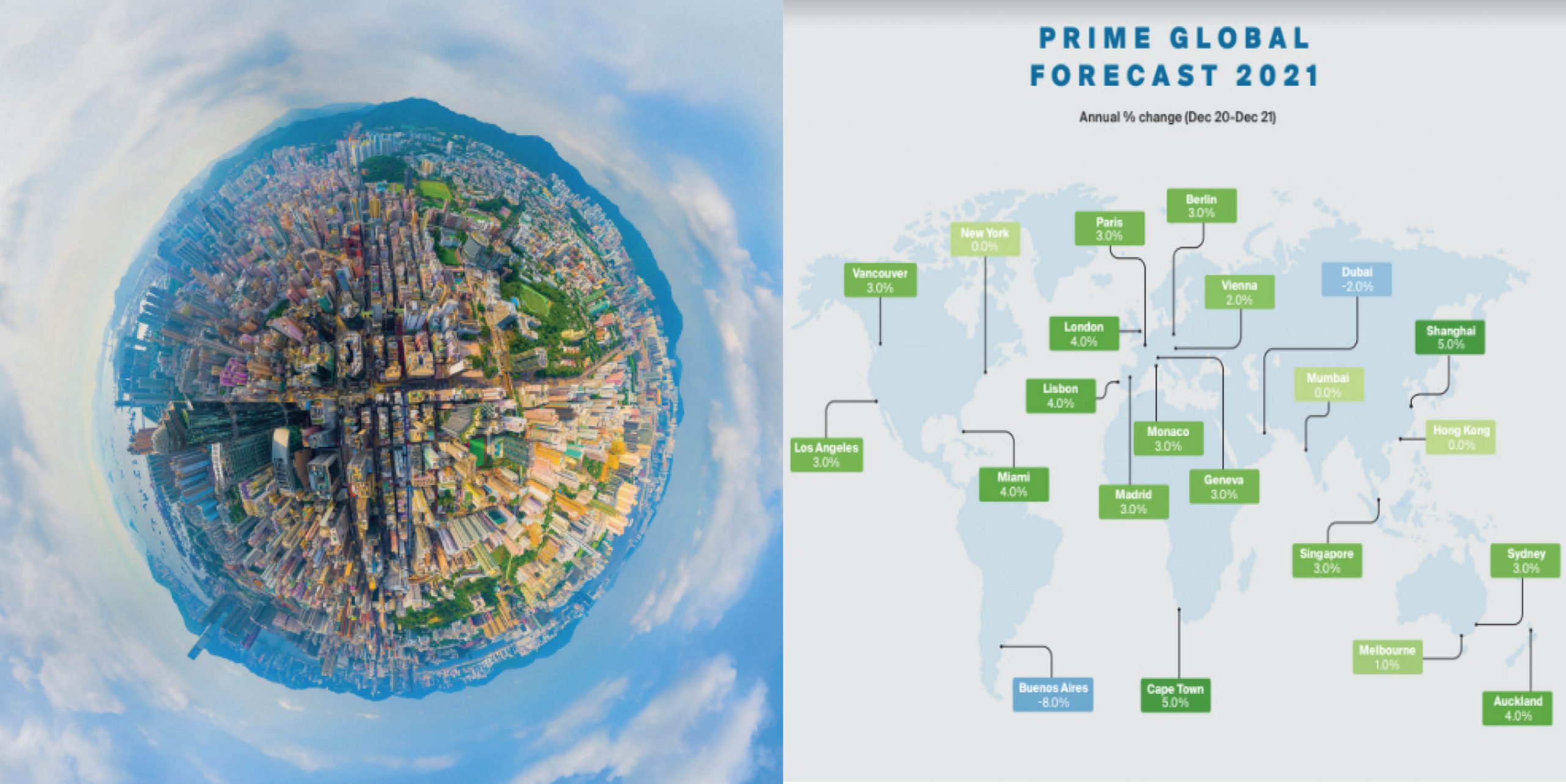

From health to economics, 2020 saw the world turned upside down by the global pandemic, however the latest data from Knight Frank’s Prime Global Cities Index suggests prime property markets were largely resilient with Cape Town and Shanghai leading the forecast for 2021 with an annual price growth of 5%.

Following the general realignment of real estate prices across the globe, the latest Knight Frank Index considers the risks and opportunities that lie ahead and highlights key trends set to influence prime residential markets in a post pandemic world.

Confirming the positive price growth forecast for the Cape Town property market, Knight Frank’s Kate Everett-Allen says, “In 2021, we expect 20 of the 22 prime global cities to see prices remain flat or increase, a slight reversal of the trend seen in 2020. A year ago, the index tracked movement in prime prices across 45 cities, rising at a rate of 1.1% per annum, by the end of September 2020 the rate had climbed to 1.6%.

Knight Frank’s prime global forecast for 2021.

Key prime market drivers in 2020/21 see the biggest risks to prime residential markets heavily affected by the pandemic and the government’s response, global and local economic performance, travel restrictions and higher taxes in income, wealth and property. How will demand, supply and sales volumes change in 2021 for Cape Town? Prime supply is forecast to remain the same with a slight rise in prime demand and prime sales.

Nick Gaertner, director and COO of Knight Frank South Africa is bullish, “The Cape Town forecast considers that we are coming off a low base. Apart from the significant impact that COVID-19 has had on the market over the last nine months, we experienced substantial depreciation of the Rand against the USD in the first half of 2020, all of which has compounded a natural price correction that has occurred in the residential market in the last two years. This correction has come off the back of a sustained 5-year period of rapid growth. While it is just a forecast at this stage and based on the assumption that South Africa will not experience another hard lockdown, prices seem to be stabilising and we expect the prime residential market to show positive growth off the new adjusted base.”

Brighter prospects

According to Everett-Allen, brighter prospects are shifting preferences from ‘safe haven assets’ such as bonds and gold towards opportunities that offer the potential of higher returns, including property.

“We could see the US dollar weaken which will shift the buying power of international investors, international travel could remain limited as there will be a staggered rollout of any vaccine globally and Oxford Economics estimates it could be 2023 before international travel returns to 2019 levels. With the potential for a quicker return to ‘normal’ this could limit unemployment and support housing markets, plus interest rates look set to remain at record lows for the foreseeable future.”

However, the index reports that 45% of prime global cities say prime sales were already back to pre-pandemic levels in Q3 2020; while 36% of cities have seen a city exodus with the suburbs the most popular destination for those relocating. Shifts were also seen in 45% of cities experiencing a large volume of expats returning home, including Cape Town, Auckland, London, New York, Singapore, Sydney, and Vancouver.

Clearly, there are challenges ahead. The concern for investors is that rents are declining in several key cities, due in part to the absence of international students, but also due to a surge in supply as landlords switched from holiday lets to long-term rentals.

Trends to monitor

According to Knight Frank’s Global Cities Index, green and ethical investing is set to filter all aspects of global property markets as the pandemic and a Biden Presidency push purpose-led investment up the global agenda.

With 9 to 5 office commuting almost a forgotten memory and digital working the new norm, there will be an online and offline approach to work and our lifestyles, leading to more residential stock in city centres and more retail and amenities in suburbs.

With many unable to reach their second homes in lockdown, and others decamping for much longer periods than usual, the location and specification of second homes is set to change, as many look for a bolthole within driving distance and the line between primary and secondary residences becomes blurred.

Investors are also considering alternative sectors. From data centres to retirement homes, and from healthcare to the private rented sector, investors are widening their net given the opportunities in the medium to long term. Overshadowed by escalating prices in prime cities since the last financial crisis, the resorts markets, whether ski or sun locations, are seeing demand strengthen.

With more countries expected to join the negative rates club in 2021, finance looks set to remain cheap, but lenders are taking a more cautionary stance, raising loan-to-value ratios and making finance costlier for highly leveraged clients.

Will governments look to raise property taxes in a post-pandemic world to replenish lost revenue or will foreign buyer taxes and bans be rolled back to help attract overseas investment? The next few months should give us some indication as to the route governments plan to take.