News

Zero-deposit and cost-inclusive home loan demand and approvals reach new peak

In addition to competitive lending by the country’s major banks in the form of attractive discounts to the prime lending rate in a still relatively low-interest rate environment, the latest data from ooba Home Loans shows a strong uptick in the demand and subsequent approval of zero-deposit (100%) and cost-inclusive (>100%) home loans.

WORDS: SUPPLIED :: PHOTOS: PEXELS

Rhys Dyer, CEO of the ooba Group says that over 56% of all home loan applications received in the first four months of 2026 fell into the zero-deposit category – two percentage points higher year-on-year. “This data may underline the lack of available deposits among homebuyers, but it also shows the banks’ willingness to enable and empower homebuyers in a tough economic climate,” says Dyer.

“For some, saving up for a deposit and covering the additional associated costs relating to a home loan are no longer viable. However, they still have the affordability and income to repay their loan on time each month, and this is where these types of loans help reduce the barrier to entry.”

Faster path to homeownership

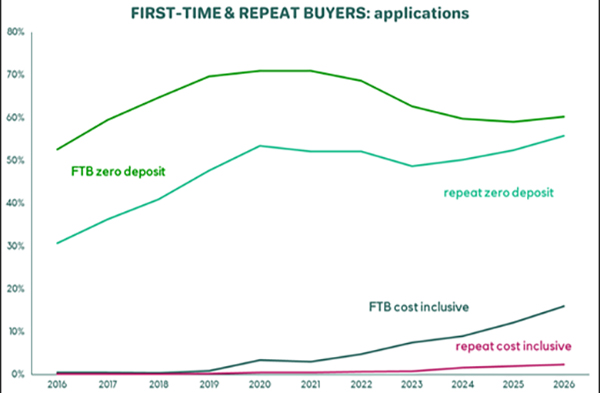

The trend is particularly pronounced among first-time homebuyers, where zero-deposit home loan applications accounted for 60.2% of all applications received from January to April 2026.

“First-time homebuyer applications for 100% home loans have remained elevated at just under 60% since 2021, while demand for >100% home loans has surged more than fivefold – from just 3% in 2021 to nearly 16% in early-2026,” says Dyer, adding that many aspiring homeowners struggle to accumulate the upfront funds required for a deposit and transaction-related costs, making cost-inclusive home loans (>100%) an increasingly attractive option.

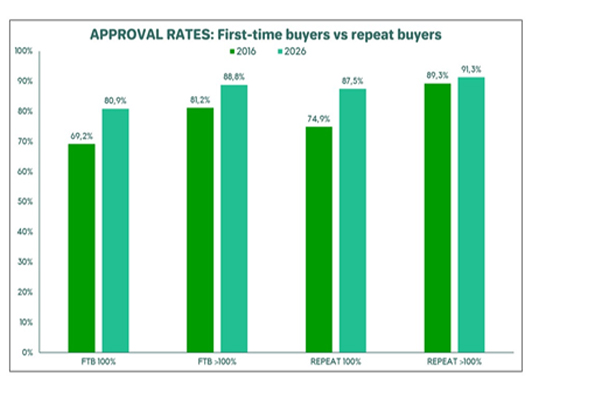

Encouragingly, the banks are not only receiving more applications for these types of loans, but are also granting them at increasingly higher approval rates. “Approval rates for 100% home loans among first-time homebuyers climbed from 69.2% in 2016 to 80.9% from January to April 2026, while cost-inclusive home loan approvals have risen even more sharply, reaching 88.8%,” says Dyer, adding that further to supporting first-time homebuyers with access to high loan to value lending, the banks are also including discounts to their bond registration costs.

At the same time the value of homes being financed through these sizeable loans has increased. “The average first-time homebuyer purchasing a property using a zero-deposit home loan paid R1.15 million in early-2026, while homebuyers accessing cost-inclusive loans paid an average of R994,297.”

Repeat homebuyers seeking – and getting – 100% home loans

Demand for zero-deposit home loans is also on the rise among repeat homebuyers. Dyer shares that applications for 100% home loans have nearly doubled over the past decade, now accounting for 55.8% of all applications received from this segment.

“While repeat buyers have traditionally relied on equity accumulated through previous property ownership to fund deposits, years of subdued house price growth – particularly in parts of Gauteng – have weakened this historical equity buffer,” he notes.

“Strained equity has also pushed more repeat buyers towards >100% home loans, which now account for 2.3% of applications.” Furthermore, Dyer emphasises that the banks generally require repeat homebuyers to fund their own costs and therefore cost inclusive lending in this segment is done on an exceptional basis.

As with first-time homebuyers, the banks have responded positively to growing demand from repeat buyers, with approval rates for 100% home loans jumping from 74.9% in 2016 to 87.5% in early-2026. Over this same period, the approval rates for cost-inclusive loans reached 91.3%.

Looking to the average purchase price of homes financed with 100% loans amongst repeat homebuyers, Dyer shares that this number reached R1.78 million in early-2026. “Our latest data signals a much lower average purchase price of R1.41 million across cost inclusive (>100%) loan applications received from this segment.”

Why the high approval rates?

Dyer says that while these figures reflect current bank lending behaviour, these loans also act as a strategic tool to help stimulate demand – particularly at a time when affordability pressures are keeping many potential homebuyers sidelined.

He adds that internal credit performance has also remained resilient, with payments in arrears by home loan applicants contained and household balance sheets among the middle-income segment appearing stable. “This positive trend is testament to the robust vetting and prequalification processes applied by companies like ooba Home Loans, ensuring that homebuyers are approved for an amount that is realistically aligned with what they can afford,” says Dyer, adding that homebuyers require a strong credit score of 661-plus to be considered for zero-deposit and cost inclusive loans.

Banks support market recovery amid uncertainty

When asked whether banks might change their stance in response to ongoing geopolitical uncertainty, including conflict in the Middle East, Dyer says there is currently little evidence of a major shift in lending behaviour, although lenders may become more cautious should global instability persist.

“For now, one thing is clear: South Africa’s banks are actively granting more 100% and >100% home loans, helping more qualified buyers access the property market and supporting housing demand in a challenging economic environment,” says Dyer.

Graphs source: ooba Home Loans